What 1,000 Tax Returns Taught Us About SBA Approvals in Early 2025

We reviewed over a thousand tax returns in the first half of 2025. Across industries, locations, and deal sizes, certain patterns came up again and again — and they weren’t subtle. If you’re a small…

We reviewed over a thousand tax returns in the first half of 2025. Across industries, locations, and deal sizes, certain patterns came up again and again — and they weren’t subtle.

If you’re a small business owner looking to raise capital, these are the three biggest insights you need to understand before you apply.

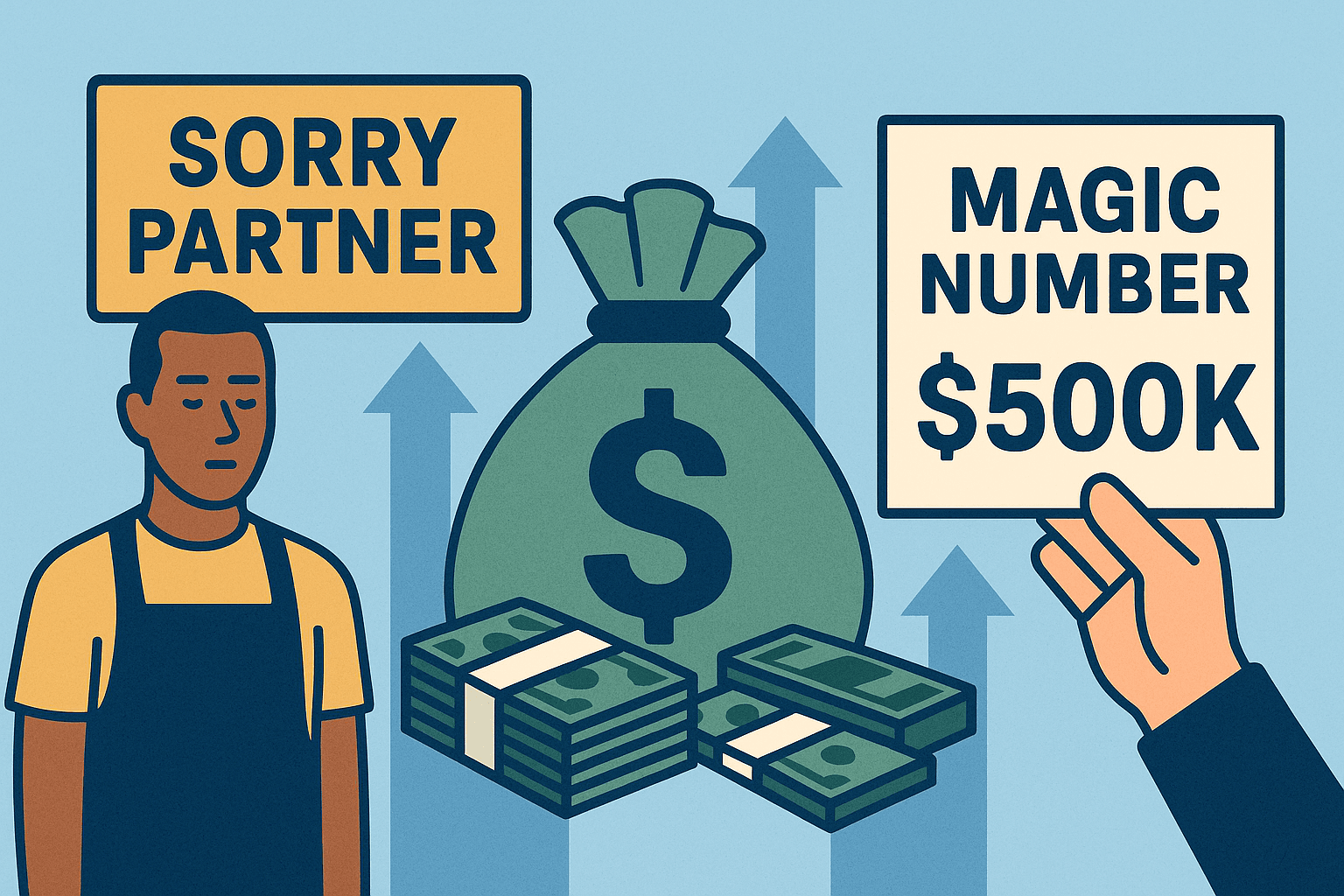

1. Sorry, Partner — Sole Owners Fund Faster

Partnerships sound good on paper. Shared responsibility, different strengths, more brainpower. But when it comes to getting approved and funded for an SBA loan?

They're a drag.

Across our dataset, sole proprietors saw their loans fund nearly twice as fast as businesses with multiple partners. Why? SBA lenders are allergic to delays — and getting every partner to sign off, upload documents, and align on terms slows the entire process down.

Smart takeaway: If you have partners, get organized before you apply. Decide who's leading the process, prep all ownership docs, and align on expectations. If you're a sole owner, lean into your speed advantage.

2. Profit Still Wins — Cashflow Is King

Revenue is great. But profit still makes all the difference.

We saw it over and over: businesses that showed a profit on their tax return were nearly 5 times more likely to get approved for financing than those that broke even or posted a loss.

It’s not that unprofitable businesses don’t get funded — some do. But when a lender sees positive cash flow, the approval conversation shifts from “can we?” to “how fast?”

Smart takeaway: Even showing a small profit changes your funding odds dramatically. If you’re close, consider how strategic tax planning could impact your next round of capital.

3. The Magic Number: $500,000 in Annual Revenue

There’s a clear threshold where SBA financing opens up: $500K in top-line revenue.

Once a business crosses this mark, nearly all the flexible, long-term, low-rate SBA products become available — especially if paired with a profit and clean ownership.

Below $500K? You’re fighting harder for approvals, and often pushed toward shorter-term, higher-cost options.

Smart takeaway: If you're approaching $500K, know that you're entering a new tier of financing access. Don't undersell your numbers, and make sure your tax returns reflect your true run rate.

The Bigger Picture

SBA lenders aren’t trying to make life difficult — but they are under pressure to de-risk. With economic uncertainty, stricter underwriting, and increasing scrutiny on defaults, they want clear, simple, fundable businesses.

The best candidates in 2025 so far?

- Sole owners

- Profitable businesses

- Revenue over $500K

If you check two or three of those boxes, you’re already in a strong position. If you don’t — it’s not game over. But your approval odds will come down to preparation, documentation, and how clearly you can tell your story.

We’ve helped hundreds of owners navigate this process. If you’re not sure where you stand, we’ll take a look — no strings attached.